When diving for value goes too far

Value investors should be careful when delving too deep for outsized returns. It turns out that the cheapest stocks by one widely used measure are not always the best.

This will come as a surprise to investors who like to rely upon price to book value as a key yardstick when making decisions. Book value is a measure of corporate net worth, and stocks that sell at low prices in comparison to their book values have traditionally been held up as bargains.

This viewpoint has been buttressed by research from Kenneth French, a professor at Dartmouth. He has found that stocks with low price-to-book (P/B) ratios handily outperform those with high P/Bs.

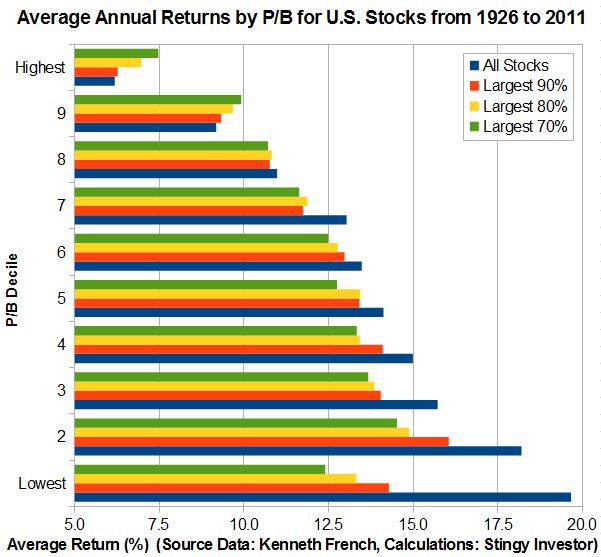

In one study Prof. French sorted stocks by P/B into 10 groups called deciles. Each group was then tracked for a year, sold, and the process repeated. The lowest P/B group performed the best with average annual returns of 19.7 per cent from 1926 to 2011. In stark contrast, the highest P/B group only gained 6.2 per cent annually. That's quite the difference and helps to explain why value investors are fond of low P/B stocks.

Could investors do even better? Generally speaking, smaller stocks have done better than larger ones over the past eight decades. So it's possible that focusing on smaller stocks with low P/Bs could produce even more impressive returns.

That's what Prof. French found. When he sorted stocks by both size and P/B, the stocks that fell in the lowest decile on both measures sported average returns of 23.5 per cent. That's an astonishingly good record.

But there is the issue of practicality. It can be hard to buy very small stocks because they tend to trade infrequently and at large spreads between bid and ask prices. That's why tiny firms are best avoided by novices.

So if you eschew small stocks, is it still a good idea to opt for stocks with the lowest P/B ratios?

The answer can be found in this accompanying graph that shows the average return of different P/B deciles for four different populations of stocks. The first uses data for all stocks. The second eliminates stocks in the smallest size decile, the third removes the next smallest decile, and the fourth drops the three smallest deciles from consideration. In this way, we can study what happens when small stocks are progressively eliminated from the return calculations.

[larger version]

The data shows that removing the very smallest stocks changes the return pattern. The lowest P/B group no-longer boasts the best returns. Instead, the second lowest P/B group is where the best returns were to be found.

What constitutes a small stock? The smallest size decile had an average market capitalization of $117-million (U.S.) as of July, 2011. The next two size deciles up had average capitalizations of $433-million and $772-million respectively.

The moral here? Since most value investors stick to stocks with market capitalizations in excess of $250-million, they should seek stocks with low but not extremely low price-to-book value ratios.

First published in the Globe and Mail, February 11 2012.

|

|