|

|||||

|

|||||

|

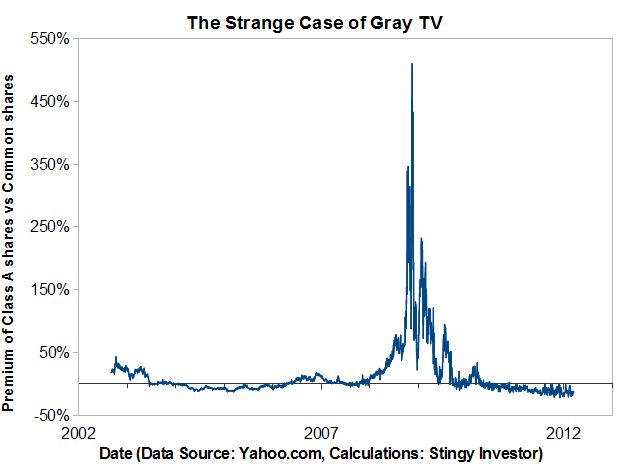

The fine art of cashing in on class differences Dual-class stocks can provide some interesting profit possibilities. If you keep an eye on the spread between the two classes of shares, and swap at the right time, you can be handsomely rewarded. It's a strategy that has its risks, but can allow you to take advantage of a market that is not quite as ruthlessly efficient as the economists would like to believe. Consider the case of Gray Television Inc. It's a small company that hails from Atlanta and operates 36 TV stations in the United States. Gray has two classes of stock. They're identical except for one difference: The A class shares (GTN.A) shares have 10 times the votes of the common shares (GTN). Therefore, it would seem that the A shares should be worth more than the common shares because of their greater voting rights. On the other hand, the common shares trade more frequently than the A shares. The extra liquidity makes them more attractive to short-term investors, who want assurance they can get in and out of the stock without trouble. No matter how these two factors interact, the preferences of investors should be relatively stable over time. That is, the spread between the common shares and the A shares shouldn't vary too much in a rational market. In practice, however, the spread between Gray's two classes of shares has been as stable as a monkey on a banana bender. Check out the wild swings in the accompanying graph.  [larger version] The A shares have traded at a discount of more than 10 per cent to the common shares on several occasions. On the other hand, they changed hands at a huge premium to the common shares after the 2008 stock-market collapse. Neither liquidity concerns nor voting rights really explain the enormous variation. The company was not in the middle of takeover talk - a factor that might give the A shares a boost - at the end of 2008. Indeed, bankruptcy seemed more likely at the time. In addition, the common shares became relatively more liquid, compared to the A shares, in late 2008 versus prior periods. It seems strange that liquidity can lead to premiums in happy times when volumes are low and to discounts in bad times when volumes are high. The simple explanation is that investors misprice stocks - even when dealing with effectively the same stock at the same time. Such anomalies are common among stocks with multiple share classes, according to a 2009 study by finance professors Paul Schultz and Sophie Shive of the University of Notre Dame. That's good news for those who want to invest in dual-class companies because they can often trade between the classes, over time, and pick up the spread. Simply moving from the expensive to the cheap class can provide a nice boost to one's long-term returns. The more adventuresome might also consider a pairs trade - in other words, buying one class while shorting the other - but this isn't always a practical possibility. Given the large number of dual-class stocks in Canada, it's worth keeping tabs on any you hold. You might be able to make a profitable swap between classes. Just keep an eye out for the bid-ask spreads and corporate developments, and trade carefully. First published in the Globe and Mail, March 24 2012. |

|||||

| |||||

| Disclaimers: Consult with a qualified investment adviser before trading. Past performance is a poor indicator of future performance. The information on this site, and in its related newsletters, is not intended to be, nor does it constitute, financial advice or recommendations. The information on this site is in no way guaranteed for completeness, accuracy or in any other way. More... | |||||