Teaching the professors how to pick good funds

Imagine standing at a podium in a lecture hall and being questioned by

100 professors for two hours. It's the stuff of student

nightmares. But that's exactly where I found myself when I recently

addressed a bevy of professors from the University of Toronto on

financial matters.

During my talk I mentioned a study I did about a decade ago on fund

fees and performance. I could recall the details only dimly but

remembered that back then Canadian equity funds managed to outperform

the market before fees - by about 0.6 percentage points a year, if

memory served - but lagged considerably after fees.

My learned audience was quite friendly but, as you might expect from a

group of professors, they wanted to know more. So I set out to update

the numbers.

My first stop: the fund filter at globefund.com. I pulled up data on

Canadian equity funds and focused on non-index open-ended funds with

five-year track records. To estimate each fund's performance before

fees I simply boosted each fund's five-year average return by its

current annual fee (usually referred to as a management expense ratio,

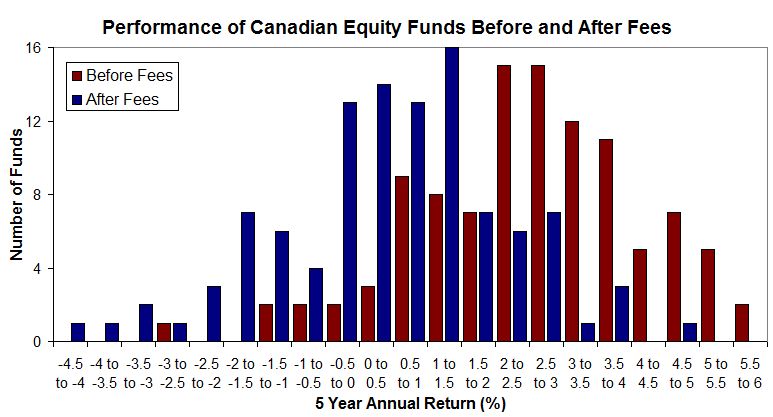

or MER). The accompanying graph shows the number of funds achieving

various (asset-weighted) return levels on both a before- and after-fee basis.

[larger graph]

Obviously fees make a big difference. On average the funds gained 2.95

per cent a year before fees and 0.96 per cent a year after fees over

the five-year period ending Oct. 31, 2011. At the same time the

S&P/TSX Composite gained an average of 2.71 per cent a year.

Before fees, the fund managers bested the index by a meagre 0.24

percentage points a year. After fees were deducted, the funds trailed

the index by 1.75 percentage points a year. In other words, despite

being smart cookies, the average manager didn't outperform by a

sufficient margin to earn back the fees they charged.

The situation might actually be even grimmer because the data has not

been adjusted for survivorship bias, which arises when poorly

performing funds are removed from the record after they are closed or

merged with other funds.

What's an investor to do? Stick to low-fee funds, of course. Index

funds are prime candidates. If you're not ready to become an indexer,

opt for lower-fee active funds. As it happens, many of the funds that

bested the index were low-fee funds. Consider, for instance, the Mawer

Canadian Equity fund, which charges a low 1.22 per cent annual fee

(MER) and managed five-year annual average performance of 3.79 per

cent.

When I'm next quizzed by a pack of professors, I'll point them to a

good low-fee fund.

First published in the Globe and Mail, December 3 2011.

|

|