|

|||||

|

|||||

|

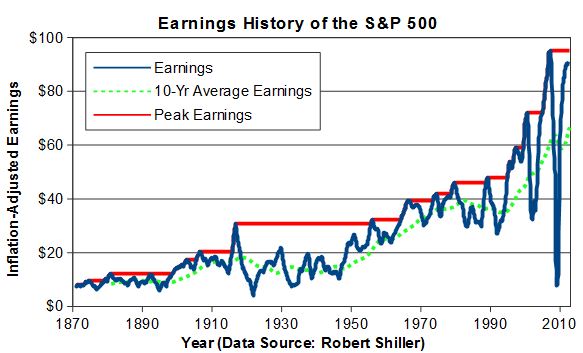

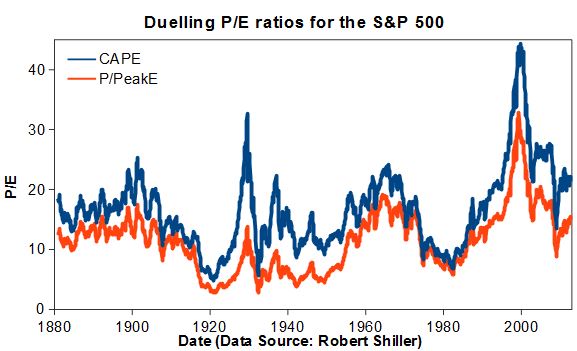

Stocks are overpriced Is the stock market overpriced? According to two ways of looking at share prices, the answer is yes. One approach, advocated by investing author Rick Ferri, measures the stock market in terms of its current price versus the peak earnings it has achieved in the past. Another approach, from Robert Shiller, an economist at Yale University, measures the market in terms of how it stacks up against the average earnings it has produced over the past 10 years. Both methods smooth out short-term fluctuations. They are useful because the standard price-to-earnings (P/E) ratio suffers from a serious flaw. The flaw arises because corporate earnings tend to plunge in recessions. As the E in P/E dwindles, the resulting ratio shoots upward. It can make stocks look expensive at the very point in the business cycle when they may actually be most attractive, just before earnings start to recover. Using peak earnings gets around this problem by keeping its eye focused on the earnings that the market has shown itself to be capable of generating, not the earnings that it is actually producing at the moment. It's a bit like assessing a baseball player in terms of his best season to date - you know he's capable of slugging 50 homers, so you don't worry too much about the slump he's in now. Prof. Shiller's approach takes a different tack. Known as the cyclically adjusted P/E ratio (CAPE), his calculation averages out peaks and valleys and gives you a sense of the market's earnings potential over a full business cycle. It's like measuring a baseball player in terms of his average production over the previous decade, rather than the most recent season. So which approach is a better measurement of the market's value? Prof. Shiller provides a public database that follows the S&P 500 and its predecessor indexes back to the 1870s, which I've used to create the accompanying graphs. The first graph shows a plot of the S&P 500's earnings history, adjusted to account for inflation, along with its peak earnings line and a rolling 10-year average earnings line.  To my eye, the rolling average does a better job of approximating the market's long-term earnings trend than the peak earnings line. Mr. Ferri's approach runs into trouble starting near the end of 1916 when the S&P 500's earnings reached an inflation-adjusted peak that was not surpassed for nearly four decades. During much of this period, earnings fluctuated at about half peak levels, which resulted in stocks looking perpetually cheap - not the best signal for anyone actually investing during this time. As a result, I'm more than a little leery of using peak-earnings based P/Es (P/PeakE) for valuation purposes. Despite my misgivings, the second graph shows both the S&P 500's CAPE and its P/PeakE over the long-term.  Today, the market's CAPE is moderately high at 21.2 while its P/PeakE comes in at 14.9. The second number might, at first glance, seem fairly low. But it's unwise to compare the two directly. Instead, compare them with their respective long-term averages. The market is 29 per cent higher than its average CAPE of 16.5, and 31 per cent higher than its average P/PeakE of 11.3. As a result, despite their differences, it turns out that both methods point to similar levels of overvaluation. Just keep in mind that such valuation estimates come with a wide range of uncertainty. They say relatively little about what the market will do over the next several months or even the next few years. Patient investors are still likely to do all right. In a recent interview, Prof. Shiller estimated that the market will deliver annualized after-inflation gains of just under 4 per cent a year. That's well short of the 6 per cent real return that blue chip stocks have produced in the past but it's well ahead of the paltry 3 per cent nominal yields available on long-term U.S. government bonds. However, achieving that 4 per cent real return may involve riding out some big ups and downs. Markets have frequently slipped to single-digit CAPE levels in the past. A move back to a CAPE of 10, without significant earnings growth, would require the market to decline by more than 50 per cent. Even lower CAPEs have been seen in the historical record. Be prepared for turbulence. First published in the Globe and Mail, November 1 2012. |

|||||

| |||||

| Disclaimers: Consult with a qualified investment adviser before trading. Past performance is a poor indicator of future performance. The information on this site, and in its related newsletters, is not intended to be, nor does it constitute, financial advice or recommendations. The information on this site is in no way guaranteed for completeness, accuracy or in any other way. More... | |||||