Tale of the tape says even value stocks are expensive

We can debate endlessly whether stock markets will soar or shrivel in

2012. But as a value investor I'm much more interested in a different

question. I want to know if value stocks are sufficiently cheap to

satisfy my inner miser.

One way to answer that question is by turning to the work of Dartmouth

Professor Kenneth French, who publishes data on U.S. stocks that goes

back to 1926. He uses price-to-book-value ratios (P/B) as a predictor

of a stock's future success.

In one study, he sorted stocks by P/B, split the market into fifths,

tracked the performance of the five groups for a year, and then

repeated the process. You can think of the lowest-P/B slice as the

value-stock group because that's where you can buy the most book value

for the lowest cost - usually because investors have fallen out of

love with these stocks and driven down their prices.

Despite their lowly status, this cluster of beaten-up stocks has been

the place to be over the long haul. The value group has generated 19.2

per cent average annual returns from July 1926 to July 2011, well

above the returns of any other group. History's lesson is clear:

buying stocks with low P/B ratios produces strong

returns. Expectations are so low for these stocks that even a little

good news is often enough to propel their prices upward.

Investors should keep in mind, though, that the line that divides the

value stock group from other stocks changes each year, as markets move

up and down. Prof. French calls this line a breakpoint and it provides

an interesting gauge of how cheap value stocks are in any given year

compared to their historical norms.

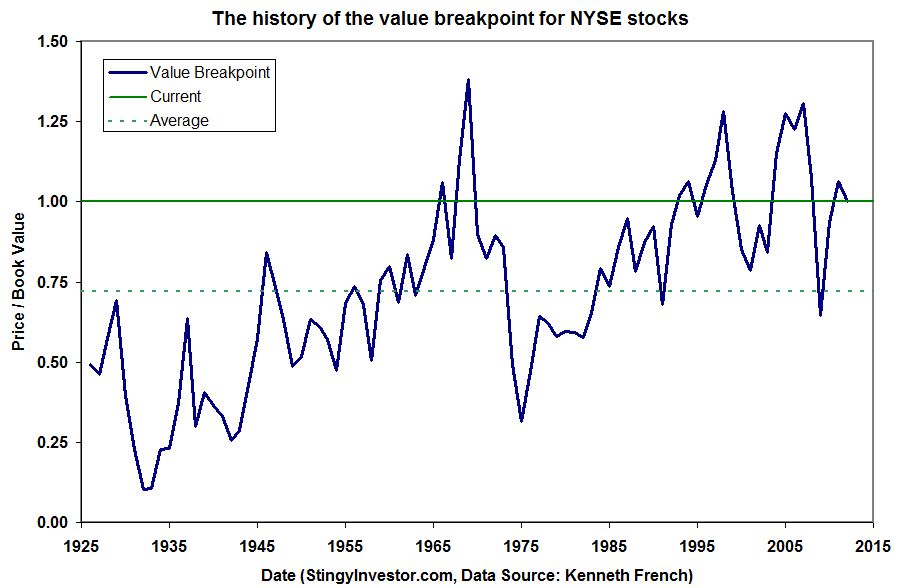

The accompanying graph shows how the value breakpoint has changed over

time. (The figures are based upon Prof. French's research, except for

the last data point, which represents my estimate of its current

level.) The graph also shows the average breakpoint for the full

period and the current breakpoint.

[Larger Version]

Over the past several decades, the value breakpoint has averaged 0.72

- stocks that have a P/B below 0.72 have fallen into the value group;

those with a P/B above this level have not. As it happens, that's

quite close to an old value investing rule of thumb that suggests

investors buy stocks only when they trade below 66 per cent of their

book value.

Unfortunately, there aren't many stocks that pass such a stringent

test this year. Indeed, the value breakpoint now sits at a P/B of

1. That's not the highest it's been in recent times but it is well

above average, which suggests that value investors should be cautious.

Don't get me wrong, I'm not rushing out to dump all my value stocks.

But as we enter 2012 I am keeping a little extra cash handy. I've

also become more demanding and have opted for the higher-quality value

stocks that are currently available.

First published in the Globe and Mail, December 31 2011.

|

|