|

|||||

|

|||||

|

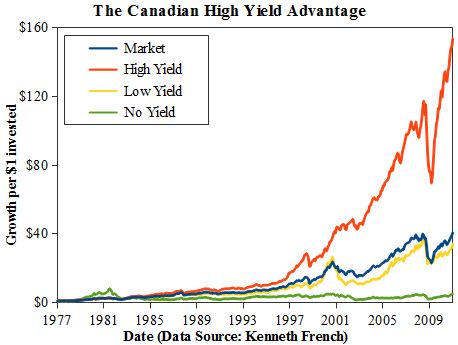

Stocks that pay you back After a topsy-turvy decade for stocks you might be finding it hard to stick to your investment plan. Perhaps you're tempted to take on more risk in an effort to make up for past losses. Maybe you're invested in only a few stocks, or those that appear to have supercharged growth prospects. Alternately, you might be cringing in fear after dumping your stocks. Problem is, taking an extreme stance - one way or the other - is likely to lead to disappointment in the long run. Instead, a balanced approach is more likely to lead to a satisfactory outcome. When it comes to stocks, take a page out of Warren Buffett's book and try to invest in good stocks for the long term. That's just the sort of approach that I recommend. Let me show you how to construct a solid do-it-yourself stock portfolio. My goal is to start new investors out on the right path and provide a few useful pointers to more seasoned aficionados at the same time. Before you begin A few words of wisdom before we launch into the stock-picking advice. It makes little sense to build an investment portfolio if you don't have a solid fiscal foundation, so thrift and debt elimination should come first. You should pay off your credit cards, lines of credit, and other debts before starting to invest seriously. After eliminating debt, sock away some cash in GICs or a high-interest savings account. If you lose your job, run into illness, or face some other calamity, you don't want this emergency fund to be in stocks. You should only turn to the markets with money that can be invested for many years. Once you're ready to invest for the long term, how should you divvy up your portfolio? Should you put all of your long-term investments in stocks, or does it makes sense to hold bonds as well? The yield generated by bonds these days is pitiful: at current inflation levels, bond investors are losing purchasing power. Taxes make the situation even worse. (Ideally bonds should be sheltered in RRSPs and TFSAs.) However, bonds are still a useful bulwark, because they offer some stability and, unlike stocks, they're unlikely to plummet in value quickly. You probably won't make much money from bonds these days, but you're not likely to lose 50% either. Stocks can't make such promises. In his book The Intelligent Investor, Benjamin Graham suggests starting with a half-and-half split between stocks and bonds in normal times. Should one or the other become attractively priced, then you might tilt the portfolio accordingly. But at a minimum, investors should have at least 25% in stocks and 25% in bonds. You might also tilt your portfolio one way or the other based on personal preference. If you're aggressive, then you might want to go 75% stocks, while more conservative investors might lean to 75% bonds. Older investors with shorter time horizons might similarly opt for more bonds than the young. But these are rules of thumb and individual circumstances might call for different allocations. The big picture Before I discuss my strategies for choosing individual companies, let's spend some time considering the overall structure of a prudent stock portfolio. To begin with, I suggest taking a page out of the Global Couch Potato approach and opting for roughly one-third in Canadian stocks, one-third in U.S. stocks, and one-third ininternational stocks. Since buying international stocks can be difficult and expensive, I suggest covering this segment with a low-cost exchange-traded fund such as the Vanguard FTSE All-World ex-US ETF (VEU), which has an annual fee of just 0.22%, or a low-fee mutual fund such as the Mawer World Investment Fund (1.49%), or perhaps a combination of the two. That leaves us with the job of picking good stocks to fill the Canadian and U.S. portions of the equity portfolio. How many good stocks? Holding just one stock could lead to great wealth, but it also has the nasty habit of ending in ruin. Just ask the people who plunged into Nortel or Bear Stearns at the wrong time. Betting on one stock means that your wealth can be subject to very wild swings, and most investors simply can't stomach the ride. Fortunately, the ride can be made smoother by adding more stocks to your portfolio. However, moving to two stocks doesn't make the ride half as wild: it only helps a bit. You've got to get up to about 10 stocks for a more substantial reduction, which is where some very aggressive professional investors stand. (The ride for these pros can still be very bumpy indeed.) So how many stocks should you include in a diversified portfolio? This is a matter of some debate, but I'm going to suggest opting for at least 20. While it can be more time-consuming to manage a large portfolio, most people are better off aiming for at least this number to avoid getting put through the volatility wringer. You can also make your portfolio more stable by favouring higher-quality firms. Similarly, the wise investor should include stocks in different industries, which enhances diversification. We'll discuss both of these ideas in more detail later. Finally, let's consider how much of each stock to buy - another concept that generates a wealth of opinions. I favour the simple philosophy of buying roughly equal dollar amounts of each. This mitigates the risk of falling in love with a particular stock and becoming blind to its faults -something that's all too easy to do. As a practical matter, it makes sense to round to the nearest 100 shares when trading, because stocks usually change hands in 'board lots' of 100 shares. Exceptions apply for stocks with very high, or very low, prices. (For instance, I don't have enough money to buy 100 shares of Berkshire Hathaway's A shares, which trade for about $120,000 a pop.) Frugal stock investors want to minimize transaction costs, fees, and taxes where possible. By picking your own stocks you save on fund fees, and that alone can make a huge positive difference in the long run. A 2.5% mutual fund fee can cut a retirement portfolio in half over the course of 30 years, all else being equal. Such is the tyranny of compounded fees. Beyond cutting fees, you also want to keep transaction costs and taxes to a minimum. To save on taxes it's often best to employ RRSPs and TFSAs. In taxable accounts, opting for strategies with long holding periods can be a good two-barrel strategy. Holding for a long time reduces trading costs and allows for tax deferral, because the tax on capital gains is postponed until you sell. As it turns out, opting for stocks you'd be happy to hold for a long time is important, because you're more likely to favour companies with staying power. This leads naturally to a more conservative approach and to larger and more mature companies. Conveniently, such firms also tend to be safer and are more likely to pay dividends. Indeed, Canadian dividend stocks are ideal for investors of more modest means, because the tax on dividends can be quite low - in some cases vanishingly small. (While the tax advantage tends to erode as income levels rise, it's hard to make sweeping generalizations. When it comes to taxes, the details matter.) It's no surprise that Canadian dividend stocks have attracted a wide and enthusiastic following based on their favoured tax status. The fundamental questions It's finally time to consider the qualities that make a stock suitable for your long-term portfolio. I like to ask two fundamental questions: 'Is it cheap?' and 'Is it safe?' In practice you'll have to compromise on both aspects. After all, you won't find a good stock being sold for nothing. Similarly, you might find a safer stock, but you'll be hard-pressed to spot one that is perfectly safe. Nonetheless, these are the guiding questions for me. They also tend to be closely related because, all else being equal, cheaper stocks are safer stocks. Now let's use these principles to screen for stocks that are both safe and cheap. We're also going to look for firms that we hope to be able to hold for a relatively long time. Dive into dividends The historical record has been kind to dividend investors, as you can see in the graph, which is based on data from Kenneth French, finance professor at Dartmouth College in New Hampshire. French splits Canadian stocks into three groups. He tracks the performance of stocks that don't pay dividends which, as you can see, have fared poorly over time. He also follows a low-yield portfolio and a high-yield portfolio. The low-yield portfolio tracks the 30% of stocks with the lowest yields each year, and the high-yield portfolio follows the 30% with the highest yields. (The portfolios are updated each year because yields change over time.) The stocks with the highest dividend yields performed the best over the long term and handily beat the market overall. On the other hand, the low-yield and no-yield groups lagged.

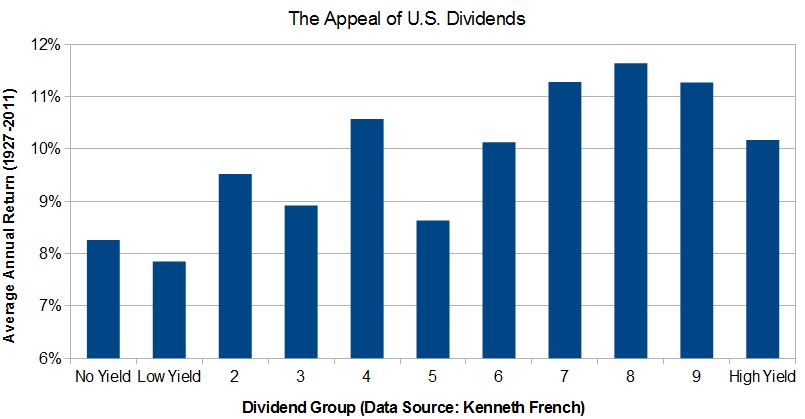

The situation is very similar south of the border as can be seen in the following graph, which presents a bar chart based on French's data. Instead of splitting stocks into three groups, he takes a sharp knife to the problem and splits U.S. stocks into eleven groups. The first group includes stocks that don't pay dividends, which delivered lacklustre results from 1927 through 2011. Stocks that paid dividends were sorted by yield and split into 10 groups called deciles. Group one contains the 10% of stocks with the lowest yields, group two the 10% of stocks with the next-to-lowest yields, and so on all the way up to group 10, which contains the stocks with the highest yields.  [Click for a larger version] The pattern of average compounded returns between the groups isn't a smooth one, but higher-yield stocks have generally done better. However, the very highest yielding group didn't take top spot, and for good reason. Exceptionally high yields can be a sign of acute distress. A stock that pays a $1 dividend per share and trades at $20 has a yield of 5%. Should it run into trouble, its share price might fall to $5, which would push its dividend to 20%. That's why I favour stocks that have high, but not super-high yields. Sticking to stocks with yields in the second, third and fourth-highest deciles is a good idea. It's a simple requirement that also happens to remove roughly 87% of Canadian stocks from consideration, so it really narrows down your choices. An eye on earnings While generous yields are a measure of cheapness, it is also important to demand safety from our stocks. Earnings are an important factor: a company that manages to earn money year in and year out is inherently safer than one with wildly fluctuating earnings. Don't get me wrong, you can still pay too much for a solid earnings record, and you can get some real deals on cyclical earners during depressed periods. But conservative investors should opt for the steady Eddies. Importantly, dividend investors hate dividend cuts, which are less likely to occur when a firm earns enough. As a result, investors should look for companies that earn more than they pay out in dividends. The ratio of dividends to earnings is called the dividend payout ratio. Investment theory suggests that firms that retain more of their earnings, and thus have low payout ratios, should grow faster than firms that pay out more in dividends. But the opposite turns out to be the case in practice. Companies that pay a large fraction of their earnings in dividends tend to grow faster than less generous companies. The need to be mindful of cash appears to make firms more resourceful whereas cash-rich companies tend to be sloppy and invest far too much in marginal ventures. I try to avoid stocks with extreme payout ratios. That means anything north of 100%. But, otherwise, high ratios shouldn't necessarily be feared. Indeed, many stocks pay more than half of their earnings to investors in the form of dividends and do quite well. But there is more to earnings and dividends than meets the eye, because both earnings and dividends can be measured on a 'trailing' basis or estimated on a 'forward' basis. Trailing measurements look at how much the company earned over the last 12 months and how much it paid out over the same period. Forward estimates try to predict how much a company will earn over the next year and how much it will pay in dividends, based on analysis or recent announcements. Ideally, earnings should exceed dividends in both cases. Mind you, analyst estimates aren't available for all stocks, and they tend to err on the optimistic side. Before moving on from earnings, I want to add in another layer of cheapness and introduce you to price-to-earnings (P/E) ratios, which are a classic measure of value. Savvy investors know that low-P/E stocks are better bargains than high-P/E stocks, all else being equal. I try to avoid stocks with ratios in excess of 20 and preferably concentrate on those with ratios under 15. Size matters Moving back to caution, conservative investors should focus on large stocks. But I'm going to be fairly lenient on this front - at least in Canada - because there aren't all that many stocks to choose from. I look for stocks with market capitalizations (shares outstanding times price per share) in excess of $500 million. I'll also stick to firms with annual sales in excess of $500 million. I boost both of these requirements to $1 billion in the U.S. due to its larger market. Dividend growth The next factor I want to consider is recent dividend growth. Firms that have boosted their dividends in the last year are particularly interesting. Ideally investors should look for dividend growth rates in excess of inflation, which currently runs near 2.5%. But I'll be lenient on this point and just require some growth. Why is dividend growth worth paying attention to? Because most companies are slow to boost their dividends. They know they'll face the wrath of investors should they cut the dividend during a soft patch. As a result, dividend increases usually happen when management thinks the firm's long-term prospects are good. Just be aware that some firms have a variable dividend policy and their payments fluctuate from quarter to quarter, or even year to year, depending on the company's results. Such policies are fine, but dividend growth in these cases has little to say about management expectations. As a result, it might not be a particularly good signal of future strength. Industry diversification I also advocate trying to build up a dividend portfolio that is reasonably diversified across industries. It turns out that opting for high-yield stocks by industry tends to give investors the benefit of diversification (reduced volatility) without costing much on the return front. Indeed, David Dreman reported in his book Contrarian Investment Strategies: The Next Generation that opting for the high-yielding stocks in each industry fared better - by about one percentage point annually - than simply going with high-yield stocks overall. But it can be hard to find stocks in every industry group that also pass the prior tests. The need to pay attention to industry diversification is particularly acute in Canada, where the stock market is dominated by financials, energy, and materials (think banks, oil companies, and mines). These three sectors make up about 78% of the S&P/TSX Composite, the best-known index of the Canadian market. Utilities, technology, and health-care firms are all woefully underrepresented in this country and amount to less than 5% of the index combined. As a result, it can be very hard to construct a truly diversified portfolio of Canadian dividend stocks, so prudent investors should consider adding non- Canadian firms to help fill in the gaps. Industry diversification is the final factor that I used to select the 20 Canadian and 20 U.S. stocks you'll find in the tables below. I tried to opt for the two highest-yielding stocks in each industry sector that pass the prior tests. But there weren't enough in each sector to fill the list, and there was an overabundance of Canadian financial stocks. As a result, I moved towards a better - although not perfect - balance by industry across all 40 stocks. Final thoughts You might think dividend investing sounds like a great approach, and I think it is. But it comes with some warts and worries. Here are a few you should keep in mind. I'm concerned that dividend investing has become extremely popular in recent years. After all, baby boomers are moving into retirement and they like income opportunities. The low yields on bonds and GICs are pushing investors towards dividends. Problem is, dividend stocks are riskier than bonds, and popularity can be the kiss of death when it comes to future returns. I'm not saying that the end is nigh for dividend investors, but stocks are not in the bargain basement either. Rather, they seem to be fully valued at the moment. I'd also advise caution when extrapolating from the past returns of Canadian dividend stocks. Why? Because our banks managed to survive the financial collapse of 2008, whereas many U.S. banks did not. (The U.S. banks burned many dividend investors badly.) Canadians also have high debt loads and a bubbly real estate market, which means it is not impossible to envision a Canadian bank failing should the economy falter. While it might be bailed out by the government, shareholders might not fare well in such circumstances - indeed, by all rights they should be wiped out. In other words, Canadian dividend investors have been lucky in recent years, so it's better to temper expectations going forward. While I hope a good dividend approach will modestly outperform over the long term, I do not expect it to trounce the markets as it has in the recent past. I would also caution that less tangible and more qualitative factors should enter into your consideration. Is a company's business in decline? Has a new competitor come into the market? Has the firm taken on too much debt? Has it been buying back shares at good prices? A thorough review of such considerations might enable you to avoid companies that are destined to disappoint. For instance, Yellow Media seemed like a solid dividend stock on most measures not that long ago. But the firm's once highly profitable Yellow Pages business wilted in the face of competition from the internet and it suffered from a debt load that proved to be too high. Regrettably, the firm recently eliminated its dividend and its share price has collapsed. Political risks can also sideswipe investors at a moment's notice. The situation in Canada seems to be stable, but you never know when it will change. Investors still remember the sudden, and painful, move by the Harper government to change the tax rates on income trusts a few years back. More than a few provincial budgets are also strained, which often leads to tax changes. South of the border matters seem more uncertain. The Obama administration has already tabled plans to boost taxes on dividends significantly. More generally, savers appear to be at the wrong end of a good deal of political rhetoric. Should Obama be re-elected, tax increases could lead to falling prices for U.S. dividend stocks. Mind you, his plans may prove to be little more than election-year posturing. Despite these worries, large dividend stocks are a great place to start. They won't make you a fortune overnight, and losses are certainly possible, but history shows that they're an excellent way to build wealth over the long term. Accompanying Stock Tables [.xls] + First Published: MoneySense magazine, April 2012 |

|||||

| |||||

| Disclaimers: Consult with a qualified investment adviser before trading. Past performance is a poor indicator of future performance. The information on this site, and in its related newsletters, is not intended to be, nor does it constitute, financial advice or recommendations. The information on this site is in no way guaranteed for completeness, accuracy or in any other way. More... | |||||